8/11/25 – We’re going to start giving assignments because this is a little ridiculous. As an article on the National Review mentioned, America is a weird country. We cannot be inventive if we lose our eccentricities. They need to remain part of who we are. America, land of the free and the weird. We are also a large country with creative corners in many cities, including rural ones. For the young peoples: Take some road trips; bring entire CD albums to share (good time to learn about prior generations’ music); drive to some midsize or, ideally, rural cities and find their artistic or simply weird sides; take pictures with both film and digital cameras. If you want an additional challenge, develop the black and white film yourself in a darkroom. Do not go on social media. You’re documenting the trip with the cameras. Review and select the best pictures later. Hint: There are many cities in the country. You should not have a hard time finding them.

Smooth Criminal

8/5/25 – We encourage everyone to take a break from whatever BS they have going on with politics and social media and do something or watch something artistic. The choreography in Smooth Criminal is so fast and complex, it’s hard to imagine anyone but Michael Jackson pulling it off. Although his backup dancers are excellent, you can’t take your eyes off of him, and it’s not because he’s in a white suit. It’s because he’s a bit more theatrical (part actor), and he understands the music more intimately. He moves in a more improvisational way, and although still quite technical and sharp, he maintains a looseness in his moves that is distinct from their more formal style (as formally trained dancers). It’s a hard balance to strike, yet he does so with seeming ease. (Frankly, he’s also more slender, so when he moves, the lines of his body are more pronounced.)

Michael Jackson – Smooth Criminal (Official Video)

8/5/25 – Here’s just one idea to help break the country out of our creative stagnation. We chose Smooth Criminal because the choreography is really inventive and brilliantly executed. It is the dance version of noir (related to literature and film). If you didn’t know this, once you have this information, you should see it in the video below.

So here is the idea: What if instead of starting with the music and adding the choreography, you start with the choreography, especially as a thematic concept but keeping it dance-able, and then create the music to fit it. Imagine you read a novel or watch a movie and then you think of dance moves that would tell the story using your body. The advantage of this approach is that music is usually accompanied by lyrics, so you’re still using words. However, this approach would force the creator to step back from the words or even sound, use the body, and then add the music to fit the choreography that is telling a story. Also, for most people in the performing arts, it would likely require more discipline and creativity. The challenge might be fruitful, as it would impose some structure and parameters to the songwriting.

Scripts, Sounds and Simplicity

7/19/25 – The novel will never die. We would like to see a revival of civilization’s ancient tradition of transmitting knowledge and history orally, such as through stories. Our native and our Jewish people are good examples of this. The written word is fixed onto material, therefore, easily reviewed, copied, and disseminated, but the oral tradition has something special – cadence. The sound of words has a power unto itself. God speaks. He doesn’t write. We write.

For example, in our native sisters’ and brothers’ beautiful oral stories, no matter where their bones may lie, their ancestors’ feet walk through their words. It is part of the stories’ beat and lends its own music to their history, culture and traditions.

The best part of God’s creation of us in his image is our own humanity in our divine complexities. Our stories, memories and mental faculties have been forged by millennia of oral tradition. Our imaginations will never die. Let us not let our oral traditions fade away and, with it, this part of our divine humanity. Let us retain the power of the spoken word. All glory and praise be to God. Thank you, Lord, for making us in your image.

7/19/25 – It is helpful to compare the written and spoken word, which has numerous expressions, to the universal system we use to transmit knowledge – our number system. It is arguably the greatest human invention in our collective history. Below is a quick, AI-generated, summary of the history of the Indo-Arabic numeral system. We cannot do math or most science orally. It must be written down, and we have a system, a language that is not spoken, to facilitate this type of knowledge and discovery. It is also universal, meaning the whole world uses the same system. Richness in language would be lost if we all spoke the same one. Richness in math and science would be hindered if we didn’t use the same system. Does our written mathematical and scientific tradition, which lacks an oral counterpart, bring us closer to or pull us farther from God? Perhaps its magnificence has the potential to delude us into thinking we could be (a) god?

“A concise overview of the Indo-Arabic numeral system, which gave us the digits 0–9 we use today:

Origins in India

• Developed in India around the 6th–7th century CE.

• Based on a decimal place-value system, which was revolutionary for its time.

• Early forms evolved from Brahmi numerals, later refined during the Gupta period.

The Invention of Zero

• Indian mathematician Brahmagupta (628 CE) was the first to treat zero as a number and define its operations.

• The concept of śūnya (void) was central to Indian cosmology and mathematics.

Transmission to the Islamic World

• Persian scholar Al-Khwarizmi introduced Indian numerals to the Islamic world in the 9th century through his work On the Calculation with Hindu Numerals.

• Islamic mathematicians adopted and refined the system, recognizing its efficiency.

Spread to Europe

• Through translations of Arabic texts, the system reached Europe by the 12th century.

• Italian mathematician Fibonacci popularized it in his 1202 book Liber Abaci, calling it modus Indorum (‘method of the Indians’).

Global Adoption

• The system gradually replaced Roman numerals due to its simplicity and power.

• Today, it’s the universal standard for arithmetic, science, and commerce.”

7/20/25 – One of the contributions that the Arabic world made to the Indian number system is to simplify the script from the Brahmi original. Although not structural in nature but more aesthetic, this helped it become the universal number system that it is today. Likewise, English is the lingua franca and uses the Roman alphabet, the Latin script, even though it belongs to the Germanic language family not the Italic (Latin) language family. India had long-standing, ancient trade routes and contact with the Middle East, and Christianity brought the Latin script to England. The Latin script, like the Arabic digits, is simple and easy to use. Therefore, one can conclude that a feature of a universal language and script will be the ease with which users can replicate its symbols.

Another interesting aspect of the cross-pollination of different languages is that Greek is really the only language that belongs to the Hellenistic language family. Relative to English or Spanish, it is spoken by few people and in a small number of countries. However, Greek is one of the key languages of the Christian Bible, and there are numerous classical texts written in it. It also has another important use – math and science. Although it is not a part of our universal number system, it is routinely used in advanced math, statistics, finance and science.

Taken together, we have the universal Indian numeral system, which uses Arabic script, the lingua franca of English, which uses the Latin script, and Greek, which also gets used in English but primarily in math, stats, finance and the sciences. The order of the universe is such that human’s creations build on each other in many ways and from various traditions. If one wants purity, it doesn’t exist because that’s not how God designed the universe. If one wants cultural domination, it also doesn’t exist because that’s not how God designed human beings. Whether we want to or not, we will ultimately end up learning from each other. So, let us as a collective civilization contribute instead of conquer. Happy Sunday, and remember God loves you with a deep and abiding love.

7/22/25 – Every nonnative English speaker that we’ve ever known has complained about the pronunciation. (Even native speakers can find the pronunciation of English words hard.) One of the contributing factors to the difficulty of English pronunciation is likely that the script changed. However, one will note that it is nonetheless the lingua franca. So, another conclusion could be that the simplicity of the script is more important than the correspondence of the script (the letter) to the sound, with the simplicity of the script and the letter-sound correspondence having an inverse relationship. This might seem strange since nonnative English speakers invariably struggle with the pronunciation, and one would think a language with accents and more consistent pronunciation would prevail as the lingua franca. However, upon deeper consideration, one doesn’t really need the script to make and to memorize the sound of words correctly. In other words, the letter-sound correspondence might end up being irrelevant since many people will end up ignoring the individual letters (or phonemes) and just focus on correctly replicating and memorizing the sound for the entire word (in its context). This brings us full circle to where we started on the importance of oral traditions. Many people likely memorized the words of the stories by sound as much as by meaning.

Unemployment, Labor Mobility and Language

One of the advantages that the United States has in comparison to India or the European Union is that, by and large, Americans all speak the same language, English, which facilitates labor mobility. (We highly encourage all Americans to learn a second language nonetheless.)

Fiscal Union, Labor Mobility and Language

The importance of speaking the same language was under-appreciated prior to Europe’s (the eurozone’s) launch of its currency and monetary union (one currency managed by one central bank) experiment, which is more commonly known as the euro. This likely resulted in labor mobility being overestimated. (Another factor of production whose mobility is important in this context is capital.)

The United States, Europe and India are all large, democratic countries or regions. However, India, unlike Europe (more specifically, the eurozone) but similar to the United States is also a fiscal union, but like Europe and dissimilar to the United States, India’s citizens speak different languages. (Although a detailed comparison of the three areas and these aspects, fiscal union and common language, are beyond the scope of this post, it is helpful to keep these similarities and differences in mind.) Thus, unlike India and Europe, the United States benefits from both a fiscal union and a common language.

The recent headlines have been focused on fiscal transfers, i.e., the federal government, which is not required to balance its budget, “bailing out” the states, with the federal government’s transfer of funds effectively being fiscal transfers between states. However, the mainstream media has not really covered labor mobility.

OCA Theory, Labor Mobility and Language

Mundell’s (1961) paper, “A Theory of Optimum Currency Areas [OCA],” presents the considerations and factors in determining whether or not an area is to be considered an optimum currency area. Mundell (p657) says, “The problem [deciding between a system of fixed exchange rates or a currency union] can be posed in a general and more revealing way by defining a currency area as a domain within which exchange rates are fixed and asking: What is the appropriate domain of a currency area?”

Mundell (p6) states that the “argument for flexible exchange rates based on national currencies is only as valid as the Ricardian assumption about factor mobility. If factor mobility is high internally and low internationally a system of flexible exchange rates based on national currencies might work effectively enough.”

On an OCA with respect to Europe, Mundell (p661) states, “One can cite the well-known position of J. E. Meade…, who argues that the conditions for a common currency in Western Europe do not exist, and that, especially because of the lack of labor mobility, a system of flexible exchange rates would be more effective in promoting balance-of-payments equilibrium and internal stability; and the apparently opposite view of Tibor Scitovsky…who favors a common currency because he believes that it would induce a greater degree of capital mobility, but further adds that steps must be taken to make labor more mobile and to facilitate supranational employment policies.”

Europe did not meet the OCA criteria, particularly labor mobility, at the time of the creation of the euro, i.e., ex-ante, and labor and, to a lesser extent, capital mobility were presumed to rise to meet the OCA criteria ex-post, after the creation of the euro. Although, capital has flowed more freely within the eurozone, the free flow of capital comes with certain risks.

For developing countries, it can pose the risk of “hot money,” i.e. destabilizing often speculative capital inflows that can evaporate when faced with an adverse condition. For an economically developed region, such as Europe, the free flow of capital can contribute to contagion. As traded securities move quickly and easily across borders, they can spread financial disruption if there are issues with those securities.

It can be argued that the creation of the euro was more beneficial to Europe’s capital than labor. European workers are often fluent in multiple languages. Yet even workers who speak different languages are limited in the countries to which they can move unless the companies for which they will be working primarily use a lingua franca, such as English, and/or the worker is able to learn the local language.

Labor Mobility and American Cities

Since Americans share a common language, it is not an issue with respect to labor mobility. Now, let us assume a symmetric natural shock, such as a pandemic, that increases the unemployment rate in each state in the country by an equal amount, say 20%. Let us also assume that half the population that is still employed is no longer required to go to an office but can work from home.

One would find that some of these people might decide to move elsewhere with a lower cost of living to decrease their living expenses even if their incomes remain the same since their barriers to doing so are limited only by their personal preferences and the costs associated with moving. Assuming constant income and lower expenses, ceteris paribus, they would have more disposable income. Thus, under the most equalizing of assumptions, workers would still likely move from areas with a higher cost of living to a lower cost of living.

Now, let us assume the same shock, but disparate unemployment rates for each state. Richter (May 22, 2020) compiled the rates here, which are “from the monthly jobs data that is based on household surveys that were collected in mid-April,” and one can see that, for April, they range from 7.9% in Connecticut to 28.2% in Nevada. His explanation for the difference is that shutting down Nevada’s large gambling and hotel industry had a strong negative impact on its economy, which seems reasonable. (The two cities have comparable population sizes and unemployment rates for February, i.e. prior to the economic shock.)

(Note, Richter states, “Since this data was collected in mid-April, it shows unemployment rates well before their peaks. The next jobs report, to be released in early June, will show the results from household surveys collected in mid-May. And those unemployment rates may be closer to the peak.”)

In a subsequent post on the same day, Richter provided an anecdote about someone he knows who moved. Once this person was no longer required to be physically present at Google’s office in Redwood City, he moved back to his parents’ house in St. Louis, Missouri, presumably to save money primarily on housing.

Richter states that for Los Angeles, the “number of working people collapsed by 23%, or by 1.16 million people, counting from December last year, to just 3.79 million workers, the lowest number in the data series going back to 1990.”

Richter adds that the “labor force…plunged by 8.3%, or by nearly 400,000 people, to 4.76 million people, the lowest since 2003. The labor force plunged because people left the county, retired, or stopped looking for work. The unemployment rate shot up to 20%.”

This is just an anecdote and early data from one city, but it is indicative of a possible trend, workers moving from cities with a higher cost of living to ones with a lower cost of living. Once more data come out, we will revisit this topic to analyze labor mobility, which is facilitated by our common language, during and (hopefully after) this pandemic period and its relationship with unemployment.

Breakdown of Fed Lending in the 2008 Crisis

A good place to start to understand the Federal Reserve’s (Fed) response to the present crisis, its unprecedented lending, is by really understanding its response to the last one, which had been unprecedented until now. Before we are able to fully analyze the Fed’s response to the present crisis, which is still evolving and ongoing, the press or public will likely need to pursue Freedom of Information Act lawsuits for release of detailed information, as Bloomberg had to do the last time. Regarding the last crisis, the most extensive analysis of the Fed’s various lending programs was done by Felkerson (2011). Therefore, this series of posts will start there, by summarizing and explaining his analysis.

As many market participants and others know, the Fed manages the federal funds rate. This is the “standard tool” (targeting the rate, not the money supply) that the Fed uses to manage the economy. The fed funds market is an uncollateralized market in which depository institutions and government sponsored enterprises lend to each other overnight. The Fed participates in this market via its primary dealers until the effective fed funds rate falls in line with the Fed’s target rate.

Also, the Fed directly sets the discount window rates and terms (duration, haircut (overcollateralization), and collateral), which is available to commercial banks and other depository institutions. These are the key rates, and they went from approximately 5+% to 0% from August 2007 to December 2008. (It is important to keep in mind that the duration and other lending terms are key features of these arrangements.)

After hitting the zero-lower bound (in terms of short-term interest rates), the Fed engaged in quantitative easing, as explained here. Regarding the Fed’s balance sheet, the assets are publicly available here, and the corresponding increases are captured on the liabilities side as reserves (or excess reserves, with interest on excess reserves (IOER) starting in October 2008).

Fed Lending Starts – General

In addition to the reduction in these short-term interest rates (as well as IOER and elaborate forward guidance), the Fed created several special facilities. As Felkerson says, “The authorization of many of these unconventional measures would require the use of what was, until the recent crisis, an ostensibly archaic section of the Federal Reserve Act—Section 13(3), which gave the Fed the authority ‘under unusual and exigent circumstances’ to extend credit to individuals, partnerships, and corporations.” This point will become even more salient when we shift to the present period.

One of the distinguishing aspects of Felkerson’s methodology is the following: “To provide an account of the magnitude of the Fed’s bailout, we argue that each unconventional transaction by the Fed represents an instance in which private markets were incapable or unwilling to conduct normal intermediation and liquidity provisioning activities…. Thus, to report the magnitude of the bailout, we have calculated cumulative totals by summing each transaction conducted by the Fed.”

“Each transaction” are the critical words. When each transaction is counted, the total lending would be considerably higher than a methodology that counts each contract, for example, repo contract since they are often rolled over, only once, depending on how each transaction is defined.

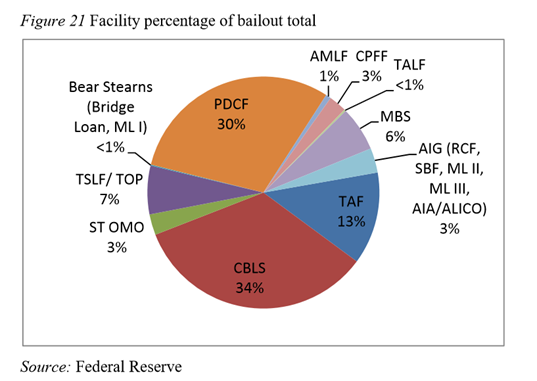

Now, the alphabet soup of lending facilities as ordered and explained by Felkerson:

- Term Auction Facility (TAF) – rate determined by auction, 28-day or 84-day term. Lending to depository institutions so that they could avoid the stigma associated with using the discount window, also acceptance of a wider range of collateral. Felkerson summarizes, “The TAF ran from December 20, 2007 to March 11, 2010…. A total of 416 unique [foreign and domestic] banks borrowed from this facility…. The Fed loaned $3,818 billion in total over the run of this program.”

- Central Bank Liquidity Swap Lines (CBLS) – “The facility ran from December 2007 to February 2010 and issued a total of 569 loans…. In total, the Fed lent $10,057.4 billion to foreign central banks over the course of this program as of September 28, 2011.” His percentages calculated for each central bank were: ECB 80%, BoE 9%, SNB 4%, BoJ 4%, All Others 3%.

- Series of term repurchase transactions (ST OMO) – “28-day repo contracts in which primary dealers posted collateral eligible under conventional open market operations…. In 375 transactions, the Fed lent a total of $855 billion dollars.”

- Term Securities Lending Facility (TSLF) – 18 primary dealers participated. Lending totaled “$1,940 billion.”

- TSLF Options Program (TOP) – 11 primary dealers participated. Lending totaled “$62.3 billion.”

Fed Lending Continued – Bear Stearns Specific

Two of Bear Stearns’ hedge funds had considerable exposure to subprime mortgages, and this led to the whole firm experiencing liquidity problems. Specifically, regardless of the quality of its collateral or the relative concentration of the troubled assets to one part of its business, the firm was shut out of the tri-party repo market, on which it depended for liquidity to operate its business.

As Felkerson writes, in response, “on March 13…[it informed the Fed] that it would most likely have to file for bankruptcy the following day should it not receive an emergency loan. In an attempt to find an alternative to the outright failure of Bear, negotiations began between representatives from the Fed, Bear Stearns, and J.P. Morgan. The outcome of these negotiations was announced on March 14, 2008 when the Fed Board of Governors voted to authorize the Federal Reserve Bank of New York (FRBNY) to provide a $12.9 billion loan to Bear Stearns through J.P. Morgan Chase against collateral consisting of $13.8 billion.”

To facilitate the actual sale to Bear Stearns, the Fed created a special purpose vehicle (SPV) called Maiden Lane I. As Felkerson explains, “Maiden Lane, LLC would repay its creditors, first the Fed [$28.82 billion] and then J.P. Morgan [$1.15 billion], the principal owed plus interest over ten years at the primary credit rate [one of the discount window rates] beginning in September 2010. The structure of the bridge loan and ML I represent one-time extensions of credit. As onetime extensions of credit, the peak outstanding occurred at issuance of the loans.”

On March 16, 2008, the same day that JPMorgan Chase issued its provisional merger with Bear Stearns, the Fed set up the Primary Dealer Credit Facility (PDCF). This facility was meant to prevent these investment banks (banks that were not eligible to go to the discount window for assistance) from experiencing liquidity issues, which could quickly become solvency issues.

I use the word “prevent,” because theoretically, that is the idea with any backstop, including FDIC deposit insurance. Its creation is meant to instill confidence, and banks only avail themselves of the facility when its mere existence is not enough to prevent a run. (All of these liquidity issues can be characterized as runs.) However, just as with the discount window, the use of these facilities can come with stigma, with investors and market participants questioning the general viability of the firm when it resorts to using the lending facility.

Felkerson summarizes the PDCF as follows: “Initial collateral accepted in transactions under the PDCF were investment grade securities. Following the events in September of that year, eligible collateral was extended to include all forms of securities normally used in private sector repo transactions…. The PDCF issued 1,376 loans totaling $8,950.99 billion…. [T]he five largest borrowers account for 85 percent ($7,610 billion) of the total. Eight foreign primary dealers would participate in the PDCF, borrowing just six percent of the total. The PDCF was closed on February 1, 2010.”

Fed Lending Continued – AIG Specific

In the wake of Lehman Brother’s bankruptcy filing on September 15, 2008, to prevent AIG from failing, the Fed first created a revolving credit facility (RCF), “on September 16, 2008, which carried an $85 billion credit line; the RCF lent $140.316 billion to AIG in total,” and the Fed created a secure borrowing facility (SBF) to facilitate repo transactions; “[c]umulatively, the SBF lent $802.316 billion in direct credit in the form of repos against AIG collateral” (Felkerson).

Then Maiden Lane II “was created with a $19.5 billion loan from the FRBNY to purchase residential MBS from AIG’s securities lending portfolio,” and these proceeds were used to pay off SBF (Felkerson).

The Fed later created Maiden Lane III to “address the greatest threat to AIG’s restructuring—losses associated with the sizeable book of collateralized debt obligations (CDOs) on which it had written credit default swaps (CDS)…, [which] was funded by a FRBNY loan to purchase AIG’s CDO portfolio, [totaling] $24.3 billion” in lending (Felkerson).

Then, “on December 1, 2009…FRBNY received preferred interests in two SPVs created to hold the outstanding common stock of AIG’s largest foreign insurance subsidiaries [AIA/ALICO transactions]… On September 30, 2010 an agreement was reached between the AIG, the Fed, the U.S. Treasury, and the SPV trustees…. [They] announced the closing of the recapitalization plan…, and all monies owed to the RCF were repaid in full January 2011” (Felkerson).

Let us pause at this point and consider that the United States central bank, whose dual mandate is price stability and full employment, and which is really not supposed to be buying anything but government-issued or, at best, government-backed (Agency MBS) securities, was purchasing CDOs of uncertain value, considerable opacity and high risk to help one corporation, AIG, which had become greedy and irresponsible. The total lending ($140 + $802 + $20 + $24 + $25) was over $1 trillion dollars. It is worth repeating. AIG got over $1 trillion in aid from the Fed while regular Americans often lost their homes, lost their jobs, went bankrupt or were plunged into poverty.

Fed Lending – The Alphabet Soup Continued

However, this was not the end of the Fed’s lending to help private industry, literally entire industries. Within the money market mutual fund (MMF) industry, the Reserve Primary Fund broke the buck on September 16, 2008. It not only held Lehman’s commercial paper but had actually increased its exposure to the firm prior to its bankruptcy.

This event triggered a run on the entire industry, which was over $2 trillion at the time. (Institution investors generally treat money market funds like depository institutions, that is, they seek capital preservation not returns.) The redemptions triggered a downward spiral in asset prices as the funds were forced to sell assets to meet them.

AMLF

The Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility (AMLF) was created on September 19, 2008 to facilitate nonrecourse loans to MMFs at the primary credit rate. “Two institutions, J.P. Morgan Chase and State Street Bank and Trust Company, constituted 92 percent of AMLF intermediary borrowing…. Over the course of the program, the Fed would lend a total of $217.435 billion…. The AMLF was closed on February 1, 2010” (Felkerson).

CPFF

The mutual fund industry’s distress resulted in a flight to safety, which had an adverse effect on the commercial paper market. With companies issuing commercial paper unable to find enough buyers, the commercial paper market froze. “To address this disruption, the Fed announced the Commercial Paper Funding Facility (CPFF) on October 7, 2008. [The SPV purchased] highly rated ABCP and unsecured U.S. dollar-denominated CP of three-month maturity from eligible issuers…. The cumulative total lent under the CPFF was $737.07 billion…. The CPFF was suspended on February 1, 2010” (Felkerson).

Note that even “highly rated ABCP” are still opaque instruments, and conservative institutional investors assess the risk of the instrument typically by the issuing bank not the underlying collateral.

TALF

These liquidity provisions were still unable to stabilize financial markets, which had transitioned to an originate-and-distribute model, and “the Fed announced the creation of the Term Asset-Backed Securities Loan Facility (TALF) on November 25, 2008. Operating similarly to the AMLF, the Fed provided nonrecourse loans to eligible borrowers posting eligible collateral, but for terms of five years. Borrowers then would act as an intermediary, using the TALF loans to purchase ABS [Asset Backed Securities]…. Although the Fed terminated lending under the TALF on June 30, 2010, loans remain outstanding under the program until March 30, 2015. The Fed loaned in total $71.09 billion” (Felkerson).

Summary of Fed Lending in 2008

Felkerson summarizes all the Fed’s lending programs as follows and provides the figure below: “When all individual transactions are summed across all unconventional LOLR [lender of last resort] facilities, the Fed spent a total of $29,616.4 billion dollars! Note this includes direct lending plus asset purchases…. Three facilities—CBLS, PDCF, and TAF—would overshadow all other unconventional LOLR programs, and make up 71.1 percent ($22,826.8 billion) of all assistance.”

Note that MBS data can be found on the SOMA site. (Felkerson separated them from the traditional Treasury securities that are a standard part of open market operations.) Felkerson notes that “[i]f the CBLS [central bank liquidity swaps] are excluded, 83.9 percent ($16.41 trillion) of all assistance would be provided to only 14 [of the largest financial] institutions [in the world]…. [And] the six largest foreign-based institutions would receive 36 percent ($10.66 trillion) of the total bailout.”

As calculated by Felkerson, the Fed’s lending programs in response to the 2008 financial crisis was massive, double the nominal GDP at the time; the institutions directly benefiting were relatively few, and the risks were high. The legal justification for what was at the time unprecedented actions was flimsy, the Federal Reserve Act—Section 13(3), if not illegal.

What was the reward for the American people, whose lives and tax dollars were ultimately at stake, for all of this Federal Reserve support for a financial system that had grown too large, too corrupt and too greedy? What did you get from the Fed’s astronomical amounts of lending? You got a system that learned how to exploit the existing order and you, the American people. The Federal Reserve has become captive to these financial players and markets, and you, the American people, are its victims.

The Dangers of Blind Ideological Adherence

The dangers of blind ideological adherence apply equally to all. They are not limited to a certain political party or economic school of thought. When one objectively analyzes the present state of affairs of the real economy, the federal government’s and the Federal Reserve’s (Fed) actions have been an unequivocal failure.

It is both obvious and correct to say that the economy is not the stock market, and the stock market is not the economy. It is also correct to observe that there has been a clear divergence in the performance of the stock market and the real economy, with the stock market far outperforming the real economy. This divergence goes well beyond the ongoing dysfunctions in financial markets. It is also a grossly immoral outcome for the American people who, by and large, live and operate in the real economy.

Therefore, it would be incorrect to conclude that the Fed, whose dual mandate is price stability and full employment, i.e. to make sure that the real economy is performing well, is meeting its mandate because the stock market is performing well. I think this is elementary logic.

Objective Premises, Ideological Conclusion

Krugman, however, arrives at just this erroneous conclusion given the same premises. To quote Krugman (2020) in his last opinion piece in the NYTimes, as of the present, “G.D.P. report for the first quarter. An economy contracting at an annual rate of almost 5 percent would have been considered very bad in normal times, but this report only captured the first few drops of a torrential downpour. More timely data show an economy falling off a cliff. The Congressional Budget Office is projecting an unemployment rate of 16 percent later this year, and that may well be an underestimate.” Thus, we are both of the mind that the present economy is terrible.

Now, Krugman’s description of the stock market, again in his own words, “Yet stock prices, which fell in the first few weeks of the Covid-19 crisis, have made up much of those losses. They’re currently more or less back to where they were last fall, when all the talk was about how well the economy was doing.”

Now, here is Krugman’s assessment of the Fed’s response to the 2008 financial crisis, and by extension and implication, his assessment of its response to the present crisis, “Now, one question you might ask is why, if economic weakness is if anything good for stocks, the market briefly plunged earlier this year. The answer is that for a few weeks in March the world teetered on the edge of a 2008-type financial crisis, which caused investors to flee everything with the slightest hint of risk.”

Krugman continues, “That crisis was, however, averted thanks to extremely aggressive actions by the Fed, which stepped in to buy an unprecedented volume and range of assets. Without those actions, we would be facing an even bigger economic catastrophe.”

Explanation of the Ideological Argument

Let us consider the argument Krugman provides. The first main point is that the Fed responded to both crises by lowering interest rates, which is the standard monetary policy response to an economic downturn no matter how it is triggered, and lower interest rates hurt bond markets and help stock markets since market participants have to put their money somewhere.

Thus, the stock market is being helped by the Fed as a “side-effect” of its efforts to help the broader economy. (A debate worth having is how the Fed can gain better traction on credit availability and terms and do so without relying so heavily on financial markets for their transmission.)

Krugman’s second main point, although not as explicitly articulated, is that the Fed, acting as the lender of last resort, should have and has done everything it can, a “whatever-it-takes” approach, to mitigate the economic damage. This is the same ideological view that ended up prevailing in the last crisis (see this previous post), and by his assessment, this approach was a wild success.

Then again, maybe not, since Krugman also states the following, “While employment eventually recovered from the Great Recession, that recovery was achieved only thanks to historically low interest rates. The need for low rates was an indication of underlying economic weakness: businesses seemed reluctant to invest despite high profits, often preferring to buy back their own stock. But low rates were good for stock prices.”

The intellectual incoherence is symptomatic of an intellectual disease that afflicts many of all ideological persuasions. It is an obstinate adherence to a set of beliefs even when the evidence clearly contradicts the ideology. Krugman knows this problem well. It could be reasonably argued that he popularized the term, “zombie economics,” which was the title of a book by John Quiggin, Zombie Economics: How Dead Ideas Still Walk among Us.

Ideologically Yours, Keynesian

In Quiggin’s words, which is what Krugman also believes, “For decades, their [market liberalism’s] advocates dominated mainstream economics, and their influence created a system where an unthinking faith in markets led many to view speculative investments as fundamentally safe. The crisis seemed to have killed off these ideas, but they still live on in the minds of many—members of the public, commentators, politicians, economists, and even those charged with cleaning up the mess.”

Instead of assessing the Fed’s performance based on a thorough, unbiased evaluation of the economy after the last crisis or in the midst of this present one, Krugman instead concludes that the Fed, headed by Jerome Powell, has done an incredible job, giving them and him an A grade. What is the basis for Krugman’s conclusion? The Fed has responded in what he considers Keynesian fashion. His is an analysis based on the application of an ideology, Keynesian economics – not on its actual outcome. This is essentially a variant of “zombie economics.” Even if the response might be theoretically correct, the form of the present (and past) application is clearly wrong because the outcome is clearly bad.

Intellectual Honesty Is Not Optional

The dangers of blind ideological loyalty and purity apply to all, including the right and the left, whether they are politicians, economists, or even Christians. In reality, when one objectively analyzes the state of affairs of the real economy, the federal government’s and the Fed’s actions have been disastrously bad.

To be a good economist or policy-maker, more broadly, a good intellectual, is to be intellectually honest. It is to have knowledge of various schools of thought and to dispassionately pick and choose from them based on what actually works. There are those among us who consider ourselves liberal economists but base our analysis not on the application of any one ideology, left, right or center, but on its actual outcome.

The outcome of the Fed intervention in the financial crisis, which was not fully disclosed to the public, was plainly and simply terrible, and the outcome of the present intervention is even worse. The data and facts speak for themselves. Lastly, the counterfactual is not redeeming when the reality is damning.

Lehman’s Lasting Legacy on the Federal Reserve

It has been only a little over a decade yet it feels like a century ago perhaps because it also feels like the latest iteration of the Gilded Age. On September 15, 2008, Lehman Brothers filed for bankruptcy. In (this summary of) his paper, Laurence Ball (2016) asks, “Why did the Federal Reserve [Fed] let Lehman Brothers fail?” He follows with, “Fed officials say they lacked the legal authority to rescue the firm, because it did not have adequate collateral to borrow the cash it needed.” He (p2) writes, “According to Bernanke (FCIC testimony, 2010): ‘[T]he only way we could have saved Lehman would have been by breaking the law, and I’m not sure I’m willing to accept those consequences for the Federal Reserve and for our systems of laws. I just don’t think that would be appropriate.’”

Ball (p2) disputes the Fed’s official line and Bernanke’s explanation. Instead, Ball concludes “that the explanation offered by Fed officials is incorrect, in two senses: a perceived lack of legal authority was not the reason for the Fed’s inaction; and the Fed did in fact have the authority to rescue Lehman.” He argues that, based on a de novo examination of its finances, Lehman did have enough collateral and that the Fed prevented it from using the Primary Dealer Credit Facility (PDCF).

The sensitivity around this question is that Lehman’s failure was a cataclysmic event for financial markets and for the global economy. If the Fed had allowed it to fail on dubious grounds, it would reflect a gross error in judgment and even incompetence. Ball (p3) states, “The record also shows that the decision to let Lehman fail was made primarily by Treasury Secretary Henry Paulson,” even though this is the Fed’s purview not the Treasury’s, and the decision was made presumably considering political sensitivities. (You might also recall that Paulson was the former chairman and CEO of Goldman Sachs, a competing investment bank, and if there were any ulterior motives, that would have been corruption.)

Therefore, the primary questions are: Why did the Fed not rescue Lehman? Did it have the legal authority to do so? Did Lehman have adequate collateral available? Were there political or other reasons for the decision?

The Complexities

In fairness to the Fed, it can get sued, and it has. Most notably, it got sued by former AIG CEO Maurice “Hank” Greenberg, who after a fair amount of drama lost his case with the court ruling that he did not have legal standing to pursue it. Instead, AIG did, and it had declined to do so. (In case you are interested in listening to Greenberg’s side of the story.) The prior ruling, in June 2015, had ruled in Greenberg’s favor but awarded no damages, and as Moyer (2017) reports the court stated that “the Federal Reserve had overstepped its authority in taking the stake in A.I.G.”

Thus, if the Fed indeed had legal concerns, the ensuing events would suggest that they were reasonable and legitimate. Also, in the United States, rehypothecation of collateral (repledging) is limited by Rule 15c3-3 of the SEC, but the United Kingdom had no such restriction. Lehman’s bailout would have included its foreign subsidiaries including its UK-based broker dealer. Thus, in terms of the counterfactual, had collateral been posted, it is uncertain who or which institution would have had final claim to it: other holders of the collateral or the Fed.

This potential concern for the Fed seems supported by Ball’s (p5) description of its actions, “The entity that Barclays almost purchased on the 14th, and which famously filed for bankruptcy on the 15th, was Lehman Brothers Holdings Inc. (LBHI), a corporation with many subsidiary companies. Most of these subsidiaries also entered bankruptcy immediately, but one did not: Lehman Brothers Inc. (LBI), which was Lehman’s broker-dealer in New York. The Fed kept LBI in business from September 15 to September 18 by lending it tens of billions of dollars through the Primary Dealer Credit Facility; after that, Barclays purchased part of LBI and the rest was wound down.” Also, LBI was heavily involved in the repo market, with its book still relatively intact perhaps due to access to the PDCF, and LBI’s disorderly unwinding might have been detrimental to the important money market.

Prior to Lehman’s failure, the Fed managed the sale of Bear Stearns, another failed investment bank, to JPMorgan Chase. The Fed subsequently set up the PDCF. (Another question that remains perhaps even more of a mystery is why Lehman did not avail itself of the PDCF earlier when its insolvency would not have been in question.) The Fed’s intervention in AIG involved a considerable equity stake, as the corporation was effectively nationalized. Thus, these two outcomes, managed sale and nationalization were not bailouts in the sense of what was to come.

Lehman – The Lesson Learned

Lehman’s bankruptcy triggered a credit crunch, and the Fed’s reaction was an alphabet soup of “special facilities,” including ones for the money market mutual fund industry, which experienced a run, and commercial paper, which froze. The Fed effectively backstopped trillion-dollar industries and provided trillions of dollars in additional support to various institutions. The knee-jerk reaction suggests that the Fed and others underestimated the impact of Lehman’s failure, and in its aftermath, decided to dramatically reverse course to a “whatever-it-takes” approach.

Lehman – The Lesson to Unlearn

The last lesson needs to be unlearned. As it turns out, what we have really learned is that moral hazard is a serious concern that has not been adequately considered or appreciated. The correct approach is to either allow firms to file bankruptcy or truly nationalize them. The focus of bailouts should be people not corporations. The American people’s tax dollars are not a piggy bank for irresponsible corporations. They are its collective contribution to build a better society for themselves.

Dramatically reversing course from what was once a more free-market ideology to a bastardized version of Keynesian economics takes the American economy and people from one extreme to another. This legacy of Lehman’s downfall is rearing its ugly head as the Fed bails out entire industries and corporations with no restraint and no accountability during this present crisis. It was irresponsible and immoral then, and it still is now. The American people deserve better.

Symmetric Storm, Asymmetric Shock and the Immorality of Fed Policy

Some have called it “the great equalizer.” In some ways, this is an accurate description. The pandemic does not discriminate, although certainly some people are more vulnerable to the disease. One could also describe the coronavirus pandemic as a symmetric storm, one that is howling across the world so fiercely that some are wondering if they are, in fact, hearing the harbinger of the apocalypse. However, the effects of the pandemic, like previous crises, are not symmetric but instead, have resulted in an asymmetric shock.

The response of the “technocratic class,” in true elitist fashion, has also been anything but symmetric. It has been a moral failure of monumental proportions. However, this is nothing new; it is just a new low. For decades, the elite in the United States and around the world have been more preoccupied with advancing their own political, academic and professional careers than about the people they are privileged with the responsibility of serving, the people whose interests they have a moral obligation to protect and to promote.

Instead, central banks and other institutions around the world have created policies that cater to the powers that be, multinational corporations and the rich. Understandably, monetary policy is difficult for many people to understand beyond basics, such as the lowering and raising of interest rates, its theoretical effects on inflation and unemployment and, perhaps, a general understanding of the mechanisms with which central banks implement the policy, what was, in the United States, known as open market operations.

Fed Response 2008

In response to the financial crisis of 2008/9, the United States central bank, the Federal Reserve (Fed), started using a set of monetary policy tools that fall under the umbrella of unconventional monetary policy. One of these policies is known as quantitative easing. It should be noted that these are experimental policies (the Japanese experience notwithstanding), and the experiment is clearly failing. Prior to the financial crisis, the Fed maintained a balance sheet that was around 800 billion.

After hitting the zero-lower-bound, meaning interest rates could not be lowered any further (aside from negative interest rates, a topic for another day), the Fed resorted to quantitative easing. They began purchasing assets not to target short-term interest rates, money market rates, such as the fed funds and the repo rates, but to lower longer-term interest rates.

Fed – Interest Rates and Morality

The Bible clearly prohibits usury, more precisely, charging interest at all; for example, “If you lend money to one of my people among you who is needy, do not treat it like a business deal; charge no interest,” Exodus 22:25, and “Do not charge a fellow Israelite interest, whether on money or food or anything else that may earn interest,” (Deuteronomy 23:19).

McCleary and Barro (2019, p11) in their book, The Wealth of Religions (support your local bookstore), wrote the following with respect to the secularization hypothesis: “Secularization applied to some aspects of John Calvin’s city of Geneva and its regulation of economic activity, especially the distinction doctrinally made between interest and usury. Interest was an economic necessity for commercial and financial transactions and was allowed by the authorities. The maximum interest rate, set at 5 percent, was regulated by the Genevan government and the Consistory, a corporate religious-moral committee of the government whose judgments were enforced by the city council…”.

Interest rates above the regulated rate were considered usurious; however, they explain that this was raised to 6.7 percent while Calvin was still living and to 10 percent after his death. With these and related actions, the city of Geneva apparently liberated itself from the theological restriction and began what they describe as “the secularization of economic activity in Geneva.”

Another way to describe it would be, thus began the unleashing of unbridled capitalism. The immorality of usury is obvious. One only has to look at its modern manifestations, such as Payday loans. Even the actions of the recently deceased former Fed Chairman Paul Volcker who raised interest rates to control inflation, an action which predictably led to a recession, should be reexamined to possibly find a better approach.

The immorality of the opposite of high interest rates, low interest rates, particularly for an extended period of time, has not been adequately discussed or perhaps even considered. Volcker’s successor, former Fed Chairman Alan Greenspan depended on this form of management to prop up financial markets and, arguably secondarily, the real economy, which has had various negative effects, such as asset price bubbles, excessive speculation and crises among others.

Fed – Bailouts

In more recent years, financial markets have become dependent not only on perpetually low interest rates but also on eye-popping amounts of central bank intervention, trillions of dollars, often in the form of “special facilities,” financial/legal vehicles that the Fed has been using to circumvent its requirement to hold only government-issued (T-bills, Treasuries, etc.) or government-backed (Agency MBS) securities. (The exact totals of “bailout” money, regardless of whether it is on the balance sheet or in special facilities, depends on how one counts it and what the Fed has been willing to disclose. It should be required to disclose it all.)

Not only are the Fed’s policies causing imbalances and other issues, but the key question is: why are the very corporations that have been causing our economic and financial problems being bailed out with trillions of dollars while the American people are suffering and being abandoned by the institutions that are supposed to be serving them? These central bank actions (both here and abroad) are exacerbating the asymmetric shock on the rich and the poor, on richer and poorer countries.

The Fed will attempt to provide pacifying, pseudo-intellectual arguments to justify these grossly immoral actions. They cannot obfuscate the truth. The institution is failing the American people whose taxes are being used in ways that are detrimental to their interests and contrary to how they should be used. This exploitation of the American people and corruption of the Fed needs to stop. The American people and people around the world deserve better from their institutions, their leaders and the “technocratic elite.”

A Great Awakening: ESG Investing Edition?

This post is part of a broader subject that very much deserves public attention and discussion. Capitalism as it has been practiced since 1776, the year Adam Smith first published his book The Wealth of Nations, coincidentally, the same year as our Declaration of Independence, is failing. It is time to accept this fact and create something different – something better.

Moral capitalism is a term and concept that has been bandied around for a while, and its full realization in all aspects of our economy, including financial markets, is long overdue. A shift to one aspect of moral capitalism has been happening to a certain extent in, of all places, the investment community, driven mainly by the demands of institutional investors.

ESG Investing

Faith-based institutions have played a considerable role in the advancement of Environmental, Social, (Corporate) Governance (ESG) investing, also known as sustainable investing, since they are particularly sensitive to the companies or industries included in their portfolios. For example, with Pope Francis’s release of the environmentally oriented encyclical Laudato Si, the Catholic Church would do well by putting words to action and decarbonizing all of its portfolios.

Although ESG investing has been gaining steam, asset managers, traditional and alternative, have been too slow in truly implementing it. Partly, this is due to a lack of data, although the EU is now leading the data collection effort, but it is also due to the managers’ lack of foresight, knowledge, skill and genuine commitment to sustainable investing.

Some investment managers have their regular funds and similar ESG funds that exclude the companies and industries that would not meet the UN PRI or the manager’s ESG criteria. This could be acceptable in the interim, until the investment community as a whole fully transitions to ESG investing, as long as managers are not simply repurposing an old fund with an ESG label and engaging in “green washing.” (Note, the institutional investors have gotten wise and can tell.) The managers need to change their underlying investment processes and, ideally, their entire culture to a responsible, long-term investment focus.

The hedge fund industry, active managers with higher fees and often a focus on absolute returns, would be wise to adopt ESG investing, since it would be a real value added, particularly as the industry needs to justify its raison d’être in a time of passive investment.

Also, a good hedge fund manager, like a traditional one, minimizes exposure to systemic risks and acts as a shield against what is often mislabeled as a black swan event. It would be hard to categorize the effects of climate change, which has been documented for at least half a century, as a black swan event.

In fact, the financial crisis was often referred to as such, when truly savvy investors saw it coming. If one was looking at the economy, the proliferation of certain financial instruments, the data, and the historical frequency with which crises have beset capitalist economies, it was hardly a black swan event.

Some might argue that many institutional investors need alpha/pure performance and any potentially “compromising” considerations, such as ESG, should be secondary at best. The premise of this argument would be that alpha and ESG are at odds. Let us consider. If all of the alpha generated over some extended period of time is wiped out as the “black swan” takes over the lagoon, then all those fees paid were effectively a waste of good money, particularly when pensions funds cannot afford to lose any money.

Additionally, the governance factor is low-hanging fruit. There has been inadequate pressure by institutional investors on management and on corporate oversight to lower executive compensation, improve the treatment and compensation of labor, include other stakeholders, such as labor, on the board of directors and to the minimize the short-term focus, including share buybacks, i.e. quarterly capitalism. I would argue that the mismanagement of these companies is often directly related to the investors’ underwhelming returns.

Nonetheless, the ESG trend is positive. Let us keep it moving forward and fix our economy so that it serves everyone. That would be moral capitalism, and that would be a great awakening.

Avarice and the Dying of the American Experiment

Americans should rage against the dying of the light that once shone from our shores as a beacon of a free and self-governing society to the world. We once held the promise of opportunity and were a source of inspiration and hope to people around the world yearning for liberty, justice and equality. Presently, we inch ever closer to becoming a failed state. At our founding, the greatest threat was a foreign one. Now, as it was for many great empires, it is a domestic one. The primary source of this internal threat is a sin as old as time – greed, which then drives corruption.

We have all heard the statistics about the growing inequality and the crony capitalism that is choking meritocracy and entrepreneurialism. It suffocates our citizens in debt and crushes their quality of life, as they run faster and faster only to move backward. This latest trend began about a half century ago. As Mishel and Wolfe (2019) stated, “From 1978 to 2018, CEO compensation grew by 1,007.5% (940.3% under the options-realized measure), far outstripping S&P stock market growth (706.7%) and the wage growth of very high earners (339.2%). In contrast, wages for the typical worker grew by just 11.9%.” And Saez and Zucman (2014) wrote, “The share of wealth held by the top 0.1 percent of families is now almost as high as in the late 1920s, when ‘The Great Gatsby’ defined an era that rested on the inherited fortunes of the robber barons of the Gilded Age.”

Under the free market capitalism model, a company’s board of directors is supposed to act as a check on irresponsible executive behavior. Instead, the boards of many companies effectively abdicate their duties and allow the executives to lavish themselves at the expense of the long-term interests of their companies. In more recent years, this is particularly evident in the stock buybacks, which have driven share prices, enriching the executives and, as usual, leaving behind the workers, who are the lifeblood of the company. (See Useem, 2019)

The callousness of the rich is particularly apparent at this precarious moment when the nation is facing a pandemic on top of the long-standing and exacerbating structural problems. Instead of putting the country’s interests first, the corporate cronies have been lobbying the GOP for a slush fund. It is not enough to undercompensate the American people for their hard work or to deprive them of secure, well-paying jobs, these parasitic corporations are now trying to siphon the American taxpayers’ money into their own pockets. As these greedy individuals and corporations continue to put their interests above the American people’s and the country’s, the country drifts further and further to plutocracy. (Also see the film series “Plutocracy,” Noble, 2019.)

- Mishel and Wolfe (2019) –

https://www.epi.org/publication/ceo-compensation-2018/ - Noble (2019) –

https://www.filmsforaction.org/watch/plutocracy/ - Saez and Zucman (2014) –

https://equitablegrowth.org/exploding-wealth-inequality-united-states/ - Useem (2019) –

https://www.theatlantic.com/magazine/archive/2019/08/the-stock-buyback-swindle/592774/

>>https://longinglogos.com/the-economic-consequences-of-the-vote/<<