Minnesota calls itself the Land of 10,000 Lakes, and Minneapolis was known for its harsh winters and its good quality of life, including its well-maintained parks and lakes. Now, it is known as the city in which George Floyd, a 46-year-old black man, was cruelly murdered by the Minneapolis police, the men and women in whom we entrust with the great privilege and responsibility of protecting and serving our communities.

The Events Resulting in George Floyd’s Murder

The purported reason for George Floyd’s arrest was a suspected $20 white-collar crime, a fraudulent payment. The real reason was the color of his skin. Thanks to Darnella Frazier, whose account Twitter suspended for an unknown reason, we have the true story, the video of George Floyd’s death, instead of the deceptive story provided in the police report. We thank Darnella, who is only 17-years-old, for her courage, conscience and presence of mind to record it. She was traumatized by the experience, and we pray for her.

George Floyd died with an officer pressing his knee against his neck for over 9 minutes. Floyd’s tortured face pressed into the asphalt, he pled with the officer(s), speaking words that brought back the memory of Eric Garner, “I can’t breathe.” “I can’t breathe,” Floyd says; “I can’t breathe.” He calls out for his mother, “mama,” he says. He urinated on himself. (The graphic video can be found on the Internet.)

There were numerous witnesses. Their panicked concern was palpable, and they begged the officer(s) to release him, to take his knee of the visibly distressed man. The officers did not. You can hear the officers joking as George Floyd is dying. Floyd’s body slowly becomes lifeless, and when the medics came, he no longer had a pulse. He was dead. (A timeline of the events is provided here. )

This is how an American citizen, our brother, a broken man (as we all are) of faith, a human being, a child of God, died. He was treated like an animal, like his life had no value, like his person had no dignity. This is how the men we gave the privilege and responsibility of protecting and serving our communities treated one of our own. They heartlessly murdered George Floyd, and we are angry; we are traumatized; we are heartbroken, and we are fed up. We want peace, justice and revolution – not just change – but a complete transformation of our society.

Our Country Is Broken

The country, which had been suffering under decades of economic mismanagement and rising inequality, reached a fever pitch under the physical and mental stress of the pandemic, the associated shutdown, and its economic devastation. The country was (and still is) a tinder box. This was the spark that lit it on fire, in many cases, literally. Since May 25, 2020, the day George Floyd was wantonly murdered by the Minneapolis Police, there have been protests.

These protests often started out peacefully but, towards evening, would erupt into violence, as a combustible mix of opportunists, anarchists, implementing a modern version of propaganda of the deed, and/or Antifa (a violence-prone, left-wing anti-fascist group) and/or white supremacists (violent right-wing groups) looted, vandalized and terrorized the city, damaging many minority-owned businesses in the process.

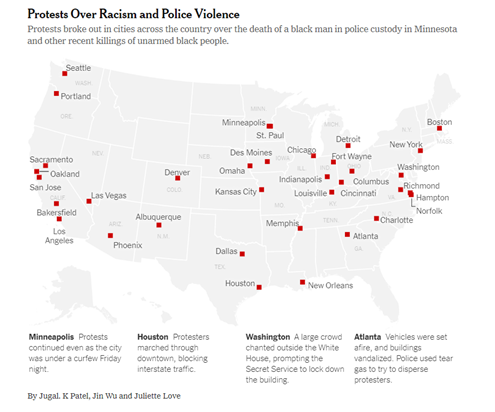

Starting Friday, May 29, 2020, the city of Minneapolis was put under curfew from 8PM until 6AM, with violations being a misdemeanor punishable by up to 90 days in jail or a $1,000 fine. On the first night of the curfew, the violence had not really abated. (Images of the protests can be found here.)

The absurdity of the autopsy report is just more proof (as if we needed it) that the problem of systemic racism in our country is not simply about the police department but also a failure of our entire system of “justice.” It is an insult to our intelligence and a disgrace to our country. As Petri wrote, “[I]t is always at the moment that their knee is descending on a human neck, or their bullet is flying toward a man, or they have him in a chokehold, when this human being’s own system decides to turn against him. It is a horrible curse.”

George Floyd to the System Reforming Itself?

The key question is: can the system reform itself, to paraphrase Cornell West, who thinks it cannot. It is understandable why he would think so. It is understandable why the people, particularly younger people, who have been completely failed by the country, its supposed leaders and its institutions, would have no faith in any system within the country being capable of self-reformation.

The justifiably angry driver says to the cop, “Dad a criminal?” Nope. “Dad a thug?” Nope. “Dad shot dead by a cop made a mistake cuz you want to come with your gun drawn.” In other words, even with protests exploding across the country in response to police brutality, as the man explains, the cop came to the car with his gun drawn over the driver not using a turn signal.

We are all too exhausted and emotionally drained to do more than try to process our pain, frustration and anger. It is hard to not feel a deep sense of despair and hopelessness about the state of our country right now. We must keep fighting though, and we have our faith to give us strength. Our deepest condolences to George Floyd’s friends and family. He was known to us, and he will be deeply missed. Fellow Americans, we say this with love – Jesus’s way – the way of peace – is the only way.

One of the advantages that the United States has in comparison to India or the European Union is that, by and large, Americans all speak the same language, English, which facilitates labor mobility. (We highly encourage all Americans to learn a second language nonetheless.)

Fiscal Union, Labor Mobility and Language

The importance of speaking the same language was under-appreciated prior to Europe’s (the eurozone’s) launch of its currency and monetary union (one currency managed by one central bank) experiment, which is more commonly known as the euro. This likely resulted in labor mobility being overestimated. (Another factor of production whose mobility is important in this context is capital.)

The United States, Europe and India are all large, democratic countries or regions. However, India, unlike Europe (more specifically, the eurozone) but similar to the United States is also a fiscal union, but like Europe and dissimilar to the United States, India’s citizens speak different languages. (Although a detailed comparison of the three areas and these aspects, fiscal union and common language, are beyond the scope of this post, it is helpful to keep these similarities and differences in mind.) Thus, unlike India and Europe, the United States benefits from both a fiscal union and a common language.

The recent headlines have been focused on fiscal transfers, i.e., the federal government, which is not required to balance its budget, “bailing out” the states, with the federal government’s transfer of funds effectively being fiscal transfers between states. However, the mainstream media has not really covered labor mobility.

OCA Theory, Labor Mobility and Language

Mundell’s (1961) paper, “A Theory of Optimum Currency Areas [OCA],” presents the considerations and factors in determining whether or not an area is to be considered an optimum currency area. Mundell (p657) says, “The problem [deciding between a system of fixed exchange rates or a currency union] can be posed in a general and more revealing way by defining a currency area as a domain within which exchange rates are fixed and asking: What is the appropriate domain of a currency area?”

Mundell (p6) states that the “argument for flexible exchange rates based on national currencies is only as valid as the Ricardian assumption about factor mobility. If factor mobility is high internally and low internationally a system of flexible exchange rates based on national currencies might work effectively enough.”

On an OCA with respect to Europe, Mundell (p661) states, “One can cite the well-known position of J. E. Meade…, who argues that the conditions for a common currency in Western Europe do not exist, and that, especially because of the lack of labor mobility, a system of flexible exchange rates would be more effective in promoting balance-of-payments equilibrium and internal stability; and the apparently opposite view of Tibor Scitovsky…who favors a common currency because he believes that it would induce a greater degree of capital mobility, but further adds that steps must be taken to make labor more mobile and to facilitate supranational employment policies.”

Europe did not meet the OCA criteria, particularly labor mobility, at the time of the creation of the euro, i.e., ex-ante, and labor and, to a lesser extent, capital mobility were presumed to rise to meet the OCA criteria ex-post, after the creation of the euro. Although, capital has flowed more freely within the eurozone, the free flow of capital comes with certain risks.

For developing countries, it can pose the risk of “hot money,” i.e. destabilizing often speculative capital inflows that can evaporate when faced with an adverse condition. For an economically developed region, such as Europe, the free flow of capital can contribute to contagion. As traded securities move quickly and easily across borders, they can spread financial disruption if there are issues with those securities.

It can be argued that the creation of the euro was more beneficial to Europe’s capital than labor. European workers are often fluent in multiple languages. Yet even workers who speak different languages are limited in the countries to which they can move unless the companies for which they will be working primarily use a lingua franca, such as English, and/or the worker is able to learn the local language.

Labor Mobility and American Cities

Since Americans share a common language, it is not an issue with respect to labor mobility. Now, let us assume a symmetric natural shock, such as a pandemic, that increases the unemployment rate in each state in the country by an equal amount, say 20%. Let us also assume that half the population that is still employed is no longer required to go to an office but can work from home.

One would find that some of these people might decide to move elsewhere with a lower cost of living to decrease their living expenses even if their incomes remain the same since their barriers to doing so are limited only by their personal preferences and the costs associated with moving. Assuming constant income and lower expenses, ceteris paribus, they would have more disposable income. Thus, under the most equalizing of assumptions, workers would still likely move from areas with a higher cost of living to a lower cost of living.

Now, let us assume the same shock, but disparate unemployment rates for each state. Richter (May 22, 2020) compiled the rates here, which are “from the monthly jobs data that is based on household surveys that were collected in mid-April,” and one can see that, for April, they range from 7.9% in Connecticut to 28.2% in Nevada. His explanation for the difference is that shutting down Nevada’s large gambling and hotel industry had a strong negative impact on its economy, which seems reasonable. (The two cities have comparable population sizes and unemployment rates for February, i.e. prior to the economic shock.)

(Note, Richter states, “Since this data was collected in mid-April, it shows unemployment rates well before their peaks. The next jobs report, to be released in early June, will show the results from household surveys collected in mid-May. And those unemployment rates may be closer to the peak.”)

In a subsequent post on the same day, Richter provided an anecdote about someone he knows who moved. Once this person was no longer required to be physically present at Google’s office in Redwood City, he moved back to his parents’ house in St. Louis, Missouri, presumably to save money primarily on housing.

Richter states that for Los Angeles, the “number of working people collapsed by 23%, or by 1.16 million people, counting from December last year, to just 3.79 million workers, the lowest number in the data series going back to 1990.”

Richter adds that the “labor force…plunged by 8.3%, or by nearly 400,000 people, to 4.76 million people, the lowest since 2003. The labor force plunged because people left the county, retired, or stopped looking for work. The unemployment rate shot up to 20%.”

This is just an anecdote and early data from one city, but it is indicative of a possible trend, workers moving from cities with a higher cost of living to ones with a lower cost of living. Once more data come out, we will revisit this topic to analyze labor mobility, which is facilitated by our common language, during and (hopefully after) this pandemic period and its relationship with unemployment.

A good place to start to understand the Federal Reserve’s (Fed) response to the present crisis, its unprecedented lending, is by really understanding its response to the last one, which had been unprecedented until now. Before we are able to fully analyze the Fed’s response to the present crisis, which is still evolving and ongoing, the press or public will likely need to pursue Freedom of Information Act lawsuits for release of detailed information, as Bloomberg had to do the last time. Regarding the last crisis, the most extensive analysis of the Fed’s various lending programs was done by Felkerson (2011). Therefore, this series of posts will start there, by summarizing and explaining his analysis.

As many market participants and others know, the Fed manages the federal funds rate. This is the “standard tool” (targeting the rate, not the money supply) that the Fed uses to manage the economy. The fed funds market is an uncollateralized market in which depository institutions and government sponsored enterprises lend to each other overnight. The Fed participates in this market via its primary dealers until the effective fed funds rate falls in line with the Fed’s target rate.

Also, the Fed directly sets the discount window rates and terms (duration, haircut (overcollateralization), and collateral), which is available to commercial banks and other depository institutions. These are the key rates, and they went from approximately 5+% to 0% from August 2007 to December 2008. (It is important to keep in mind that the duration and other lending terms are key features of these arrangements.)

After hitting the zero-lower bound (in terms of short-term interest rates), the Fed engaged in quantitative easing, as explained here. Regarding the Fed’s balance sheet, the assets are publicly available here, and the corresponding increases are captured on the liabilities side as reserves (or excess reserves, with interest on excess reserves (IOER) starting in October 2008).

Fed Lending Starts – General

In addition to the reduction in these short-term interest rates (as well as IOER and elaborate forward guidance), the Fed created several special facilities. As Felkerson says, “The authorization of many of these unconventional measures would require the use of what was, until the recent crisis, an ostensibly archaic section of the Federal Reserve Act—Section 13(3), which gave the Fed the authority ‘under unusual and exigent circumstances’ to extend credit to individuals, partnerships, and corporations.” This point will become even more salient when we shift to the present period.

One of the distinguishing aspects of Felkerson’s methodology is the following: “To provide an account of the magnitude of the Fed’s bailout, we argue that each unconventional transaction by the Fed represents an instance in which private markets were incapable or unwilling to conduct normal intermediation and liquidity provisioning activities…. Thus, to report the magnitude of the bailout, we have calculated cumulative totals by summing each transaction conducted by the Fed.”

“Each transaction” are the critical words. When each transaction is counted, the total lending would be considerably higher than a methodology that counts each contract, for example, repo contract since they are often rolled over, only once, depending on how each transaction is defined.

Now, the alphabet soup of lending facilities as ordered and explained by Felkerson:

Term Auction Facility (TAF) – rate determined by auction, 28-day or 84-day term. Lending to depository institutions so that they could avoid the stigma associated with using the discount window, also acceptance of a wider range of collateral. Felkerson summarizes, “The TAF ran from December 20, 2007 to March 11, 2010…. A total of 416 unique [foreign and domestic] banks borrowed from this facility…. The Fed loaned $3,818 billion in total over the run of this program.”

Central Bank Liquidity Swap Lines (CBLS) – “The facility ran from December 2007 to February 2010 and issued a total of 569 loans…. In total, the Fed lent $10,057.4 billion to foreign central banks over the course of this program as of September 28, 2011.” His percentages calculated for each central bank were: ECB 80%, BoE 9%, SNB 4%, BoJ 4%, All Others 3%.

Series of term repurchase transactions (ST OMO) – “28-day repo contracts in which primary dealers posted collateral eligible under conventional open market operations…. In 375 transactions, the Fed lent a total of $855 billion dollars.”

Two of Bear Stearns’ hedge funds had considerable exposure to subprime mortgages, and this led to the whole firm experiencing liquidity problems. Specifically, regardless of the quality of its collateral or the relative concentration of the troubled assets to one part of its business, the firm was shut out of the tri-party repo market, on which it depended for liquidity to operate its business.

As Felkerson writes, in response, “on March 13…[it informed the Fed] that it would most likely have to file for bankruptcy the following day should it not receive an emergency loan. In an attempt to find an alternative to the outright failure of Bear, negotiations began between representatives from the Fed, Bear Stearns, and J.P. Morgan. The outcome of these negotiations was announced on March 14, 2008 when the Fed Board of Governors voted to authorize the Federal Reserve Bank of New York (FRBNY) to provide a $12.9 billion loan to Bear Stearns through J.P. Morgan Chase against collateral consisting of $13.8 billion.”

To facilitate the actual sale to Bear Stearns, the Fed created a special purpose vehicle (SPV) called Maiden Lane I. As Felkerson explains, “Maiden Lane, LLC would repay its creditors, first the Fed [$28.82 billion] and then J.P. Morgan [$1.15 billion], the principal owed plus interest over ten years at the primary credit rate [one of the discount window rates] beginning in September 2010. The structure of the bridge loan and ML I represent one-time extensions of credit. As onetime extensions of credit, the peak outstanding occurred at issuance of the loans.”

On March 16, 2008, the same day that JPMorgan Chase issued its provisional merger with Bear Stearns, the Fed set up the Primary Dealer Credit Facility (PDCF). This facility was meant to prevent these investment banks (banks that were not eligible to go to the discount window for assistance) from experiencing liquidity issues, which could quickly become solvency issues.

I use the word “prevent,” because theoretically, that is the idea with any backstop, including FDIC deposit insurance. Its creation is meant to instill confidence, and banks only avail themselves of the facility when its mere existence is not enough to prevent a run. (All of these liquidity issues can be characterized as runs.) However, just as with the discount window, the use of these facilities can come with stigma, with investors and market participants questioning the general viability of the firm when it resorts to using the lending facility.

Felkerson summarizes the PDCF as follows: “Initial collateral accepted in transactions under the PDCF were investment grade securities. Following the events in September of that year, eligible collateral was extended to include all forms of securities normally used in private sector repo transactions…. The PDCF issued 1,376 loans totaling $8,950.99 billion…. [T]he five largest borrowers account for 85 percent ($7,610 billion) of the total. Eight foreign primary dealers would participate in the PDCF, borrowing just six percent of the total. The PDCF was closed on February 1, 2010.”

Fed Lending Continued – AIG Specific

In the wake of Lehman Brother’s bankruptcy filing on September 15, 2008, to prevent AIG from failing, the Fed first created a revolving credit facility (RCF), “on September 16, 2008, which carried an $85 billion credit line; the RCF lent $140.316 billion to AIG in total,” and the Fed created a secure borrowing facility (SBF) to facilitate repo transactions; “[c]umulatively, the SBF lent $802.316 billion in direct credit in the form of repos against AIG collateral” (Felkerson).

Then Maiden Lane II “was created with a $19.5 billion loan from the FRBNY to purchase residential MBS from AIG’s securities lending portfolio,” and these proceeds were used to pay off SBF (Felkerson).

The Fed later created Maiden Lane III to “address the greatest threat to AIG’s restructuring—losses associated with the sizeable book of collateralized debt obligations (CDOs) on which it had written credit default swaps (CDS)…, [which] was funded by a FRBNY loan to purchase AIG’s CDO portfolio, [totaling] $24.3 billion” in lending (Felkerson).

Then, “on December 1, 2009…FRBNY received preferred interests in two SPVs created to hold the outstanding common stock of AIG’s largest foreign insurance subsidiaries [AIA/ALICO transactions]… On September 30, 2010 an agreement was reached between the AIG, the Fed, the U.S. Treasury, and the SPV trustees…. [They] announced the closing of the recapitalization plan…, and all monies owed to the RCF were repaid in full January 2011” (Felkerson).

Let us pause at this point and consider that the United States central bank, whose dual mandate is price stability and full employment, and which is really not supposed to be buying anything but government-issued or, at best, government-backed (Agency MBS) securities, was purchasing CDOs of uncertain value, considerable opacity and high risk to help one corporation, AIG, which had become greedy and irresponsible. The total lending ($140 + $802 + $20 + $24 + $25) was over $1 trillion dollars. It is worth repeating. AIG got over $1 trillion in aid from the Fed while regular Americans often lost their homes, lost their jobs, went bankrupt or were plunged into poverty.

Fed Lending – The Alphabet Soup Continued

However, this was not the end of the Fed’s lending to help private industry, literally entire industries. Within the money market mutual fund (MMF) industry, the Reserve Primary Fund broke the buck on September 16, 2008. It not only held Lehman’s commercial paper but had actually increased its exposure to the firm prior to its bankruptcy.

This event triggered a run on the entire industry, which was over $2 trillion at the time. (Institution investors generally treat money market funds like depository institutions, that is, they seek capital preservation not returns.) The redemptions triggered a downward spiral in asset prices as the funds were forced to sell assets to meet them.

AMLF

The Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility (AMLF) was created on September 19, 2008 to facilitate nonrecourse loans to MMFs at the primary credit rate. “Two institutions, J.P. Morgan Chase and State Street Bank and Trust Company, constituted 92 percent of AMLF intermediary borrowing…. Over the course of the program, the Fed would lend a total of $217.435 billion…. The AMLF was closed on February 1, 2010” (Felkerson).

CPFF

The mutual fund industry’s distress resulted in a flight to safety, which had an adverse effect on the commercial paper market. With companies issuing commercial paper unable to find enough buyers, the commercial paper market froze. “To address this disruption, the Fed announced the Commercial Paper Funding Facility (CPFF) on October 7, 2008. [The SPV purchased] highly rated ABCP and unsecured U.S. dollar-denominated CP of three-month maturity from eligible issuers…. The cumulative total lent under the CPFF was $737.07 billion…. The CPFF was suspended on February 1, 2010” (Felkerson).

Note that even “highly rated ABCP” are still opaque instruments, and conservative institutional investors assess the risk of the instrument typically by the issuing bank not the underlying collateral.

TALF

These liquidity provisions were still unable to stabilize financial markets, which had transitioned to an originate-and-distribute model, and “the Fed announced the creation of the Term Asset-Backed Securities Loan Facility (TALF) on November 25, 2008. Operating similarly to the AMLF, the Fed provided nonrecourse loans to eligible borrowers posting eligible collateral, but for terms of five years. Borrowers then would act as an intermediary, using the TALF loans to purchase ABS [Asset Backed Securities]…. Although the Fed terminated lending under the TALF on June 30, 2010, loans remain outstanding under the program until March 30, 2015. The Fed loaned in total $71.09 billion” (Felkerson).

Summary of Fed Lending in 2008

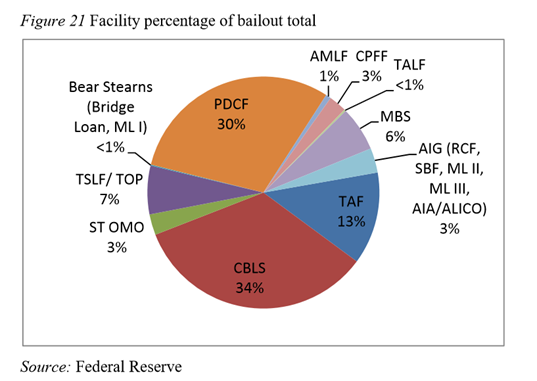

Felkerson summarizes all the Fed’s lending programs as follows and provides the figure below: “When all individual transactions are summed across all unconventional LOLR [lender of last resort] facilities, the Fed spent a total of $29,616.4 billion dollars! Note this includes direct lending plus asset purchases…. Three facilities—CBLS, PDCF, and TAF—would overshadow all other unconventional LOLR programs, and make up 71.1 percent ($22,826.8 billion) of all assistance.”

Note that MBS data can be found on the SOMA site. (Felkerson separated them from the traditional Treasury securities that are a standard part of open market operations.) Felkerson notes that “[i]f the CBLS [central bank liquidity swaps] are excluded, 83.9 percent ($16.41 trillion) of all assistance would be provided to only 14 [of the largest financial] institutions [in the world]…. [And] the six largest foreign-based institutions would receive 36 percent ($10.66 trillion) of the total bailout.”

As calculated by Felkerson, the Fed’s lending programs in response to the 2008 financial crisis was massive, double the nominal GDP at the time; the institutions directly benefiting were relatively few, and the risks were high. The legal justification for what was at the time unprecedented actions was flimsy, the Federal Reserve Act—Section 13(3), if not illegal.

What was the reward for the American people, whose lives and tax dollars were ultimately at stake, for all of this Federal Reserve support for a financial system that had grown too large, too corrupt and too greedy? What did you get from the Fed’s astronomical amounts of lending? You got a system that learned how to exploit the existing order and you, the American people. The Federal Reserve has become captive to these financial players and markets, and you, the American people, are its victims.

Many of us might feel understandably powerless right now, as we face numerous hardships. A dangerous pandemic is costing hundreds of thousands of lives. At present, there have been at least 240,000 deaths from it worldwide. Our democracy is slipping away. The person who has taken over the White House is evil, greedy, corrupt and traitorous, as are his cronies, who have taken over our government.

The economy is being destroyed, as Cohen and Hsu (2020) report, “more than 33 million people have joined the unemployment rolls in seven weeks…. [E]conomists expect the monthly jobs report on Friday to put the April unemployment rate at 15 percent or higher — a Depression-era level.”

Our planet is also being destroyed by greed and consumerism. Global climate imbalances are yielding strange results, such as plagues of locusts, murder hornets, and a polar vortex is forecast to hit the Northeast in the next couple days while the West is set to experience record heat.

White “vigilante justice” seems to go unchecked while black men are being subjected to modern-day lynching. More generally, the lives of black and brown people are being valued less than others. They are being treated as second-class citizens and have to operate under a different set of standards than other Americans.

Our social fabric is being eroded in other ways, as people have abandoned religious institutions, many of which have forsaken the path of Jesus and instead of worshiping God have been worshiping worldly things. Their hypocrisy and the general misguided nature of secularism has driven people into the arms of other false gods, such as paganism, scientism, or cult-like leaders, such as Richard Dawkins.

Younger people, in particular, are frustrated, as the changes they want are frequently thwarted often by older people, the people who should care about them, or the political or economic establishment, the institutions that should care about them. These are dark times for the nation and for the world, and it can all feel so hopeless.

Jesus’s Divine Power

However, for Christians and for the world, there is one great hope, one eternal light to which we can fix our fortunes and our spirits – Jesus Christ. Mathis (2020) writes, “In the final tally, Jesus stands alone. No other human has left such a deep and enduring impression on the world, and he did so in only three years of active public life.” This is an indisputable truth. No other person has had anywhere near the impact that Jesus has had.

Where did Jesus’s power come from? As Christians, we would answer from God, as he is one with the Father. For non-Christians, the broad details of Jesus’s life are the following. He was a poor Jew from Galilee, who was born in Bethlehem. He had a mere 12 Apostles. He had no social media platform, with no hoard of followers. He wrote nothing, not a single word. He had no degrees or certifications. He had no worldly titles, wealth, power or prestige (aside from being of the line of David). Jesus spoke words, and he performed miracles. He was crucified, and he rose from the dead.

Those who believe him to be a mere mortal might ask: how could his one life have transformed the world more than any other, and what insight might that provide regarding our current challenges?

Man’s False Power

The reality is that those with power now, like the Caesars of their day, will be largely forgotten or will become a cautionary tale for others aspiring to be like them and for those who are inclined to be seduced by them. None of us can predict the future, but one thing is certain: no human present or future will compare at all with the power Jesus has now and will continue to have.

Some Christians are handwringing about the state of the faith, its trajectory, particularly in the West, and the rise of secularism. They have little faith and need to have more of it in God’s plan. They need to trust him more. They need to focus on glorifying God and not themselves. They need to stop compromising their morality and Christianity for political expediency or a false sense of power. Real power rests in Jesus, in God, and we only have access to real power when we rest in him.

The Benefits of Jesus’s Power

The benefits of Jesus’s power as it resides in us is peace and hope. In our darkest hours, we can turn to him, to our Lord and our God, and know that we are loved. If we entrust in him our lives, his power becomes our power. One might ask: how does this translate in practical ways in the real world?

A feeling of peace and hope helps one continue to fight another day. One needs to keep the faith and fight the good fight until the end. God gives us that resilience. Our faith in Jesus is our strength, and as Christians, we should never forget that. We should also share his power manifested in us with others during our shared trials and tribulations. With this, we will be and will do what we are called to do – be the salt and light of the world.

“You are the salt of the earth. But if the salt loses its saltiness, how can it be made salty again? It is no longer good for anything, except to be thrown out and trampled underfoot. You are the light of the world. A town built on a hill cannot be hidden. Neither do people light a lamp and put it under a bowl. Instead they put it on its stand, and it gives light to everyone in the house. In the same way, let your light shine before others, that they may see your good deeds and glorify your Father in heaven” (Matthew 5:13-16). Amen.

A person in a negative is hard to see. Similarly, a person defined in the negative is hard to understand. To be simply and honestly Christian is to define oneself in a straight-forward and positive way: we are Christ-followers. Define who you are by defining what you are for. Are you for Jesus? If you say “yes,” then he has to be at the center of everything in your life. By everything, I mean everything.

Not in the Negative – Christian in the Positive

In this essay, Mattson (2020) highlights what we should all know and be clear about as Christians. He writes, “One of the hallmarks of following Christ is emulating his life. And this is what Christianity essentially is: Jesus. Christianity isn’t a political ideology, or a sovereign nation, or a set of laws legislating values or enforcing a society’s preferred brand of morality. Christianity is centered upon Christ.”

Instead of a positive self-definition, many Christians have fallen into this trap of negative self-definition, often leaving Christ behind as they refer to the world in which they are too much involved. Some are opposed to abortion and same-sex marriage. Some are opposed to immigrants and non-whites. Some are opposed to, more generally, “liberal culture.” The list is long, tedious, and unhelpful.

Jesus denounced immorality and hypocrisy, but he was not defined by his opposition to these things or to the Jewish religious establishment and its corruption. Instead, what defined him was what he advocated, what he taught, what he asked of us, what he said and did. This is what we follow and try to emulate.

If you are about children and families, as most people are, by the way, then actually support families. Help poor families raise their children out of poverty. If you are about a certain cultural position, say traditional marriage, then support that cause. Broken black families, in particular, could benefit from real support from Christians, meaning financial, psychological and spiritual support.

Instead of chastising others who do not fit your worldview – help those that do. If you are opposed to immigrants and non-whites, you really need to revisit Jesus’s teachings because there is no support in them for those positions. If you are opposed to “liberal culture” or “conservative culture,” how do you define those cultures? This one exercise in definition might not be as straight-forward as you might expect.

The Negative Is More Dangerous for Non-Christians

For non-Christians, the negative trap is even more dangerous. There is no one example to which they can set their compass, no star of Bethlehem, as Christians have in Jesus. They are stranded on a vast ocean, water everywhere yet not a drop to drink. What good is water if one cannot drink it, if it cannot sustain life? We have the water of life. We just have to have faith in the Word, and it will flow.

Non-Christians have to not just define themselves in the positive, as we do, but first, they have to determine what the positive actually is. What does the positive look like? Some atheists say that they do not like organized religion because it makes people into robots. Having a clear and positive self-definition as Christ-followers have in Jesus is not turning someone into an automaton. Instead, it is similar to the difference between a photo and its negative.

We are made in God’s image, and we have a clear image of God as man – an image in the positive. As any good Christian knows, emulating Jesus is hard. We will fail and fail again. We ask our God and each other for forgiveness. In this process, we become more aware of our own particular weaknesses and vulnerabilities, which we also take to the Lord in prayer to help us overcome them. There is nothing robotic in this lifelong spiritual journey. It is as individual as the prints on our hands and feet, as we are.

What is robotic, however, is looking to a stronger central government for direction on personal conduct, which really needs to be developed the hard way, that is character formation through individual introspection and reformation, and in the aggregate, a cultural unity that is as thin as the government’s decrees.

This is where Europe went astray. Its people, tired of the religious wars and their religious institutional failures, effectively abdicated morality to the government. However, governments are ill-suited for a task so complex and profound and are also even more prone to corruption than the church is while lacking a stable corrective mechanism as the church has. As argued here, Jesus Christ’s teachings are indelible and immutable; a nation’s laws are not. Once a bad leader rises to power, the country’s laws can be changed, and the leader can be hard to overthrow.

It is tempting but unproductive to define oneself by everything one is against, that is in the negative. Define what you are for, and then do the hard work of committing to those things and fighting for them. Put your time, talent and treasure into those efforts. This applies to Christians and non-Christians alike. The difference is that, for Christians, we have a clear picture – in the positive – of what that should look like.

The dangers of blind ideological adherence apply equally to all. They are not limited to a certain political party or economic school of thought. When one objectively analyzes the present state of affairs of the real economy, the federal government’s and the Federal Reserve’s (Fed) actions have been an unequivocal failure.

It is both obvious and correct to say that the economy is not the stock market, and the stock market is not the economy. It is also correct to observe that there has been a clear divergence in the performance of the stock market and the real economy, with the stock market far outperforming the real economy. This divergence goes well beyond the ongoing dysfunctions in financial markets. It is also a grossly immoral outcome for the American people who, by and large, live and operate in the real economy.

Therefore, it would be incorrect to conclude that the Fed, whose dual mandate is price stability and full employment, i.e. to make sure that the real economy is performing well, is meeting its mandate because the stock market is performing well. I think this is elementary logic.

Objective Premises, Ideological Conclusion

Krugman, however, arrives at just this erroneous conclusion given the same premises. To quote Krugman (2020) in his last opinion piece in the NYTimes, as of the present, “G.D.P. report for the first quarter. An economy contracting at an annual rate of almost 5 percent would have been considered very bad in normal times, but this report only captured the first few drops of a torrential downpour. More timely data show an economy falling off a cliff. The Congressional Budget Office is projecting an unemployment rate of 16 percent later this year, and that may well be an underestimate.” Thus, we are both of the mind that the present economy is terrible.

Now, Krugman’s description of the stock market, again in his own words, “Yet stock prices, which fell in the first few weeks of the Covid-19 crisis, have made up much of those losses. They’re currently more or less back to where they were last fall, when all the talk was about how well the economy was doing.”

Now, here is Krugman’s assessment of the Fed’s response to the 2008 financial crisis, and by extension and implication, his assessment of its response to the present crisis, “Now, one question you might ask is why, if economic weakness is if anything good for stocks, the market briefly plunged earlier this year. The answer is that for a few weeks in March the world teetered on the edge of a 2008-type financial crisis, which caused investors to flee everything with the slightest hint of risk.”

Krugman continues, “That crisis was, however, averted thanks to extremely aggressive actions by the Fed, which stepped in to buy an unprecedented volume and range of assets. Without those actions, we would be facing an even bigger economic catastrophe.”

Explanation of the Ideological Argument

Let us consider the argument Krugman provides. The first main point is that the Fed responded to both crises by lowering interest rates, which is the standard monetary policy response to an economic downturn no matter how it is triggered, and lower interest rates hurt bond markets and help stock markets since market participants have to put their money somewhere.

Thus, the stock market is being helped by the Fed as a “side-effect” of its efforts to help the broader economy. (A debate worth having is how the Fed can gain better traction on credit availability and terms and do so without relying so heavily on financial markets for their transmission.)

Krugman’s second main point, although not as explicitly articulated, is that the Fed, acting as the lender of last resort, should have and has done everything it can, a “whatever-it-takes” approach, to mitigate the economic damage. This is the same ideological view that ended up prevailing in the last crisis (see this previous post), and by his assessment, this approach was a wild success.

Then again, maybe not, since Krugman also states the following, “While employment eventually recovered from the Great Recession, that recovery was achieved only thanks to historically low interest rates. The need for low rates was an indication of underlying economic weakness: businesses seemed reluctant to invest despite high profits, often preferring to buy back their own stock. But low rates were good for stock prices.”

The intellectual incoherence is symptomatic of an intellectual disease that afflicts many of all ideological persuasions. It is an obstinate adherence to a set of beliefs even when the evidence clearly contradicts the ideology. Krugman knows this problem well. It could be reasonably argued that he popularized the term, “zombie economics,” which was the title of a book by John Quiggin, Zombie Economics: How Dead Ideas Still Walk among Us.

Ideologically Yours, Keynesian

In Quiggin’s words, which is what Krugman also believes, “For decades, their [market liberalism’s] advocates dominated mainstream economics, and their influence created a system where an unthinking faith in markets led many to view speculative investments as fundamentally safe. The crisis seemed to have killed off these ideas, but they still live on in the minds of many—members of the public, commentators, politicians, economists, and even those charged with cleaning up the mess.”

Instead of assessing the Fed’s performance based on a thorough, unbiased evaluation of the economy after the last crisis or in the midst of this present one, Krugman instead concludes that the Fed, headed by Jerome Powell, has done an incredible job, giving them and him an A grade. What is the basis for Krugman’s conclusion? The Fed has responded in what he considers Keynesian fashion. His is an analysis based on the application of an ideology, Keynesian economics – not on its actual outcome. This is essentially a variant of “zombie economics.” Even if the response might be theoretically correct, the form of the present (and past) application is clearly wrong because the outcome is clearly bad.

Intellectual Honesty Is Not Optional

The dangers of blind ideological loyalty and purity apply to all, including the right and the left, whether they are politicians, economists, or even Christians. In reality, when one objectively analyzes the state of affairs of the real economy, the federal government’s and the Fed’s actions have been disastrously bad.

To be a good economist or policy-maker, more broadly, a good intellectual, is to be intellectually honest. It is to have knowledge of various schools of thought and to dispassionately pick and choose from them based on what actually works. There are those among us who consider ourselves liberal economists but base our analysis not on the application of any one ideology, left, right or center, but on its actual outcome.

The outcome of the Fed intervention in the financial crisis, which was not fully disclosed to the public, was plainly and simply terrible, and the outcome of the present intervention is even worse. The data and facts speak for themselves. Lastly, the counterfactual is not redeeming when the reality is damning.